Tracy Stone-Manning, Biden Nominee for Bureau of Land Management, Takes Large Loan and Likely Impermissible Gift from Donor & Developer

Tracy Stone-Manning, Joe Biden’s nominee to head the highly influential Bureau of Land Management took a large previously undisclosed loan of an indeterminate amount from a wealthy land developer when she was a Congressional staffer. There are serious questions raised by this loan including whether the developer received special treatment from the loan, whether Mrs. Stone-Manning had recused herself from proceeds regarding the developer, whether she complied with the Congressional Gift Rules prohibiting gifts to staff, and whether she properly disclosed the loan to government agencies and borrowers. The Senate must take a close look at Mrs. Manning’s finances to ensure that the questionable loan does not permanently imperil her ability to be an impartial and effective servant of the American people.

Background

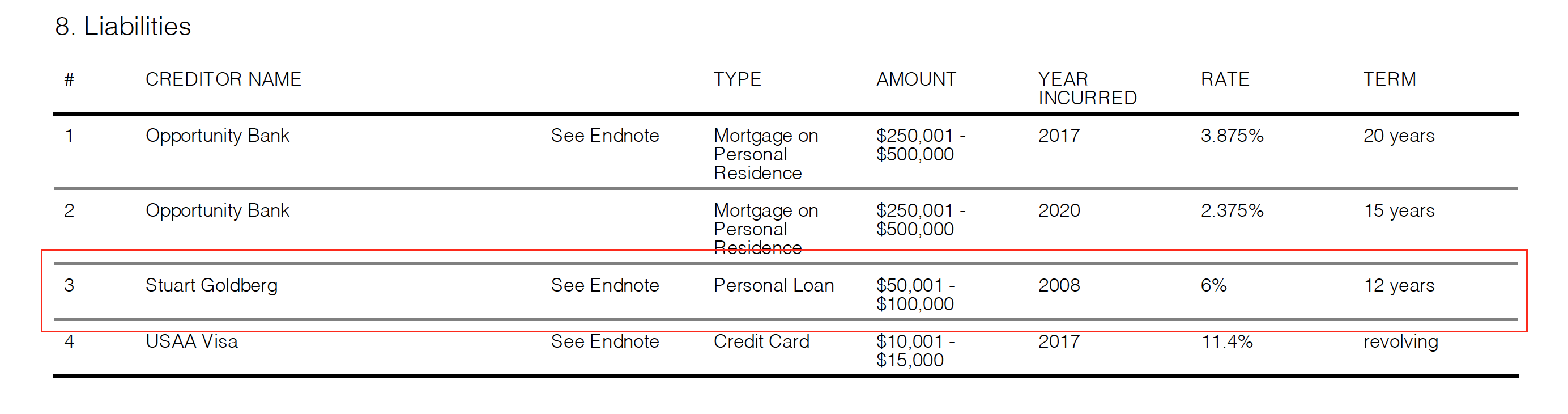

On her financial disclosure to the Office of Government Ethics as part of her nomination process, Tracy Stone–Manning disclosed that she recently paid off a loan which had an outstanding principal value of between $50,000 and $100,000. She states that she paid the loan in full in 2020.

From her Office of Government Ethics Form 278:

The guidance for filers of OGE Form 278 notes clearly that the value reported should be the highest value during the reporting period.

Amount: Mark the appropriate category of amount or value. For revolving charge accounts, use the value of the liability at the end of the reporting period. For all other liabilities, mark the category that corresponds to the highest value of the liability during the reporting period.

For Mrs. Stone-Manning this would indicate that the outstanding principal on the loan was at least $50,000 during the reportable period, which began in January 2020. The most favorable assumption for Mrs. Stone-Manning is that she had an outstanding loan balance of $50,000 on January 1, 2020.

Numerous Unanswered Questions Raised by the Loan

How Much was the Original Loan for?

Stone-Manning’s Form 278 indicates that she had a principal balance of not less than $50,000 no earlier than January 1, 2020. She also states that the loan originated in 2008 and was for twelve years. Under the most generous assumptions this would assume the last payment (the 144th payment) was in December of 2020.

The outstanding balance number is important, because due to the fact that Stone-Manning was never a highly paid Congressional staffer required to file a financial disclosure, and Montana does not have personal disclosure requirements for gubernatorial staff, the information on the Form 278 is the only information we have about this loan.

If this was a traditional personal loan where a borrower makes regular equal sized payments over the term of the loan (twelve years, or 144 monthly payments) the original size of the loan would have had to be approximately $450,000. The table below (click here for the underlying calculations) outlines what the payment schedule would have to had look like for this to be a twelve year six percent loan.

| Annual Interest Rate | 6% | |||

| Years | 12 | |||

| Payments Per Year | 12 | |||

| Amount | $450,000 | |||

| Payment Number | Monthly Payment | Interest Payment | Principal Payment | Outstanding Principal |

| 1 | $4,391.33 | $2,250.00 | $2,141.33 | $447,858.67 |

| 12 | $4,391.33 | $2,129.24 | $2,262.09 | $423,585.54 |

| 24 | $4,391.33 | $1,989.72 | $2,401.61 | $395,541.89 |

| 36 | $4,391.33 | $1,841.59 | $2,549.73 | $365,768.58 |

| 48 | $4,391.33 | $1,684.33 | $2,707.00 | $334,158.91 |

| 60 | $4,391.33 | $1,517.37 | $2,873.96 | $300,599.62 |

| 72 | $4,391.33 | $1,340.11 | $3,051.22 | $264,970.47 |

| 84 | $4,391.33 | $1,151.92 | $3,239.41 | $227,143.80 |

| 96 | $4,391.33 | $952.12 | $3,439.21 | $186,984.05 |

| 108 | $4,391.33 | $739.99 | $3,651.33 | $144,347.35 |

| 120 | $4,391.33 | $514.79 | $3,876.54 | $99,080.90 |

| 132 | $4,391.33 | $275.69 | $4,115.64 | $51,022.52 |

| 144 | $4,391.33 | $21.85 | $4,369.48 | ($0.00) |

The scenario presented above seems difficult to reconcile when it is noted that at the time of the origination of the loan in 2008, Mrs. Stone-Manning, according to the data from the Secretary of the Senate maintained at the website Legistorm, only earned $59,104 in 2008. If this were a traditional personal loan, it would have consumed approximately $52,692 per year in debt payments, more than Mrs. Stone-Manning’s total take home pay from the Senate.

If this were a traditional personal loan, it would have consumed approximately $52,692 per year in debt payments, more than Mrs. Stone-Manning’s total take home pay from the Senate.

Was This Interest Rate an Impermissible Gift?

As the table above shows, at the rate of six percent, the loan would have consumed all of Mrs. Manning’s take home income. Nonetheless, assuming she could afford the loan payments, and other household expenses, from her husband’s income or other income streams, was the loan rate an impermissible gift under the rules of the United States Senate?

The rules of the Senate state that it is only permissible for staff to take “loans from banks and other financial institutions on terms generally available to the public.”All indications are that this loan was a personal loan, and was not collateralized. If this is the case, then the most appropriate analogue would the going rate for credit cards or personal loans at the time, which were in Q1 of 2008 we between 11.8% and 11.1%.

This five per cent delta is extremely significant. If the scenario of Mrs. Stone-Manning paying the loan in even installments over 12 years were accurate, then the total cost of the loan decreases by $179,952 over the life of this loan, from $812,303 to $632,350.

This implicates the loan as an impermissible gift because the amount of benefit is substantial, $179,952, not de minimis, and the loan rates were not widely available to the public at 6% at that time. Further the below market rate loan is not permissible as a gift from a friend under Senate ethic rules because the Senate have very clear standards for allowing gifts:

In determining whether a gift is provided on the basis of personal friendship, the Member, officer, or employee shall consider the circumstances under which the gift was offered, such as:

- The history of the relationship between the individual giving the gift and the recipient of the gift, including any previous exchange of gifts between such individuals.

- Whether to the actual knowledge of the Member, officer, or employee the individual who gave the gift personally paid for the gift or sought a tax deduction or business reimbursement for the gift.

- Whether to the actual knowledge of the Member, officer, or employee the individual who gave the gift also at the same time gave the same or similar gifts to other Members, officers, or employees.

Unless the Mr. Goldberg and Mrs. Stone-Manning had regularly exchanged gifts of tens of thousands of dollars it is difficult to conceive of this as a gift that was part of their normal and customary personal relationship.

Further the Senate requires written pre-approval for gifts exceeding $250 in value. Since approval from Senate Ethics would immediately immunize Mrs. Stone-Manning from criticism for this loan, and she has produced no such letter, it seems reasonable to assume that this was not pre-approved by the Senate Ethics committee.

For all of these reasons it seems clear that Mrs. Stone-Manning receiving a below market rate loan was clearly impermissible under the rules of the Senate.

How Did a Modestly Compensated Government Employee Qualify for Such a Significant Loan or Was it a Much Smaller Loan that was Never Repaid?

As noted above, Mrs. Stone-Manning earned less than sixty-thousand dollars in 2008. There is no evidence that her or her husband had particularly lucrative income sources outside of her employment in the Senate. Land records in Montana seem to confirm that they were of middle class means, showing them to have purchased a modestly priced home in March of 2009 for $257,400.

They sold the property for $279,000 two years later, making a modest profit of likely around $20,000 after fees.

They sold the property for $279,000 two years later, making a modest profit of likely around $20,000 after fees.

This is important because it is helpful to underscore that they were not in a financial position where they would otherwise qualify for a $450,000 personal loan.

The obvious question becomes did Mrs. Stone-Manning receive this loan because of her position in the Senate and the anticipation that she would likely be a leading policy maker in Montana in the future whose friendship and gratitude would be valuable.

Mrs. Stone-Manning borrowed the funds from Stuart Goldberg who is an affluent developer in Montana. Considering that conservation and land development are heavily regulated and Mrs. Stone-Manning even at the time of the loan was an influential voice in Montana politics and policy, and a clearly rising star, it is reasonable to question whether Mr. Goldberg rightly perceived that a below market loan to Mrs. Stone-Manning was a wise investment in an individual who could be part of the decision making process for Mr. Goldberg’s business ventures. Further, even if she were not a decider, Mrs. Stone-Manning was seen as an individual who would be close to the policy makers, notably, the state’s Governor and Senator, and could be in a position to persuade them on Mr. Goldberg’s behalf.

Was This Even Really a Loan?

As the table above shows, if this was a normal personal loan with equal monthly payments, it would have had to been for a shockingly large amount, over $450,000. A more reasonable conclusion is that whatever transaction occurred between Mr. Goldberg and Mrs. Stone-Manning was more of a gift, than a loan transaction. There are some facts that are known that lead one to believe that this was not a loan.

First, the term of the loan is extremely convenient. The Form 278 lists the loan as having a twelve year term. This is not a standard term in the lending industry and just happens to coincide with the duration of time between when the loan was given, 2008, and when Mrs. Stone-Manning was being vetted to serve in the Biden Administration, late 2020.

Further, Mrs. Stone-Manning is no longer of such modest means as she was when a younger Senate Staffer, last year she was paid $168,838, likely more than enough to have been able to close out a $50,000 personal loan, particularly since it was at a higher rate than she was paying on her home mortgage, making it economically irrational not to close out the 6% debt and take on greater debt in her home which she recently refinanced at 2.375 rate, less than half the rate that she was supposedly paying on her loan to Mr. Goldberg. It was also lower than the rate she financed her home at when she purchased it in 2017.

It is reasonable to ask, whether Mrs. Stone-Manning only suddenly closed out this loan because she was facing a confirmation hearing. If the loan had been forgiven by Mr. Goldberg, government ethics staff would likely have instructed her that she would have had to have paid taxes on that loan when it was forgiven. As the Internal Revenue Service notes,

In general, if you have cancellation of debt income because your debt is canceled, forgiven, or discharged for less than the amount you must pay, the amount of the canceled debt is taxable and you must report the canceled debt on your tax return for the year the cancellation occurs.

If Mrs. Stone-Manning had let this note be forgiven, amending previous tax returns to pay the taxes owed would have been a problematic red flag for her confirmation, and could have been construed as tax evasion.

A more likely scenario is that the loan was for approximately $28,000 in 2008 and was never really repaid, but when suddenly confronted with a Senate Confirmation, Mrs. Stone-Manning had post-hoc calculated what should have been paid if she was paying 12 years worth of six percent interest, the going interest rate in late 2020/early 2021, and paid that amount to “settle” the debt.

Ethical and Legal Questions that Remain Unresolved

If this debt was still a real obligation for Mrs. Stone-Manning during her tenure in government it raises additional serious questions.

- Did Mrs. Stone-Manning cut off all communication in her official capacity with Mr. Goldberg, and his business associates, when she served in state and federal government?

- Did Mrs. Stone-Manning inform Senator Tester that she received a massive personal loan from a wealthy individual – one who donated to him in the past?

- Did Senator Tester cut off official communication with Mr. Goldberg following Mrs. Stone-Manning securing the loan, or at least exclude her from all official office interactions with Mr. Goldberg?

- When Mrs. Stone-Manning was Director of DEQ or Chief of Staff for former Governor Bullock, did Mr. Goldberg have any pending business in front of the state, and did Mrs. Stone-Manning in writing instruct her staff to ensure her recusal from any decisions she might make involving Mr. Goldberg or his business interests?

- If this were a real debt, did Mrs. Stone-Manning disclose it to her mortgage lenders when she was applying for a loan?

- If it were a traditional personal loan with even monthly payments, then it was an extremely large loan and would seem to make it difficult for the Stone-Mannings to qualify for the mortgages they secured.

- If the loan was in fact forgiven and the Stone-Mannings did not pay taxes on it, have they violated state and federal tax laws?

Unless Mrs. Stone-Manning is able to answer these questions clearly for the Senate there could be a serious ethical cloud hanging over her confirmation.